Market Commentary Brian Stutland

Brian Stutland

Brian Stutland With today’s sell off in US equities accelerating we have been getting questions from about how we are managing downside risk. Our primary risk management tool is our proprietary SVIX (“synthetic VIX”), which allows us to replicate the performance of the VIX without the decay found in other long volatility vehicles like VXX. One strategy clients have been very pleased with is our Low Volatility Large Cap strategy, in which we aim to meet or exceed the S&P 500’s returns with a fraction of the downside volatility. We recommend this strategy to clients who would traditionally own large cap stocks but want to remove the tail risk of black swan market crashes.

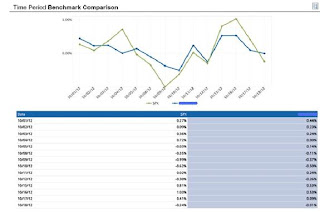

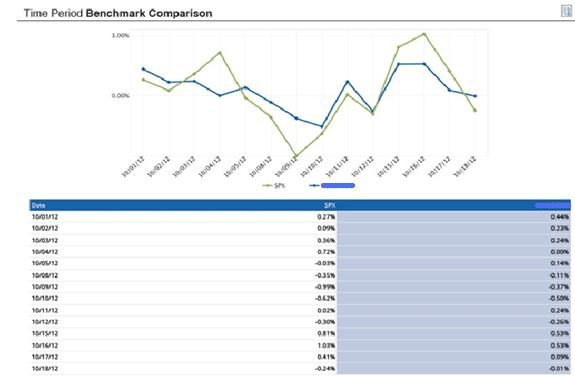

We achieve our target performance via an actively managed portfolio of stock options and an allocation to SVIX. Below is the performance of this strategy month to date, which as you can see has matched the S&P 500’s return with a fraction of the volatility.

Joe Tigay

Joe Tigay